A few thoughts and trades Mr. Blonde is focused on given the current environment and start of Fed tightening cycle. Refer to Don’t Fight the Fed for more detail.

The BTD bros will be out this week, but history suggests directional market returns should be less the focus when Fed tightening cycle ensues. The pace and slope of market returns flattens (like the curve) which increases importance of portfolio structure and alpha. A few ideas:

Style Driven Stock Screen

This is an idea screen and not designed to be a backtest or intended to traded as a group. The objective is to filter a larger US universe to find stocks with fundamental characteristics that historically proven to be resilient during the start of Fed tightening cycles.

The result of the screen is 65 stocks meeting the following criteria.

Technical note: factor exposure reflects cross-sectional sector neutral z-score of a given fundamental characteristic. For example, a reading of +1.0 on current value suggests the company is one standard deviation cheaper than the sector average (i.e. peer group).

Sector Neutral Factor exposure:

Current value > -0.5

Profitability > -0.25

Growth/Momentum > -0.25

Risk > 0

FCF / EV > 0

Price momentum > -0.5

Estimate Revisions > -0.25

For context, the average stock on this list was down -0.2% last week vs. S&P 500 -1.2%. Over the last month the average stock is -0.8% vs. S&P 500 -2.4%.

As the recent market volatility dust settles, Mr. Blonde expects participants to focus on resilience and relative strength given a backdrop that will remain uncertain and choppy — a feature of Fed tightening cycles.

Stocks catching Mr. Blonde’s attention here include: HD, WMT, PG, MO, UNH, JNJ, TMO, DHR, ABBV, ANTM, HCA, WAT, MAS, MSFT, ORCL, ACN, AMAT, CSCO, PSA, CBRE.

Boring is Beautiful

With elevated market volatility and likely more to come as Fed moves down a tightening path now is a good time to focus on ‘boring’ parts of the market. When market volatility is high you don’t need high beta positions to exacerbate your PnL volatility.

MSCI minimum volatility ETF (USMV) has massively underperformed over the last two years, but as the volatility outlook changes it is sensible to expect low volatility (i.e. boring) parts of the market to perform better from here.

The group weightings of low volatility ETFs will be far less cyclical than S&P 500, which already has relatively low cyclical group weighting. Also notice the difference in group weights between MSCI and S&P offerings. Historically, the relative performance between the two has trended together, but can differ in finite periods of time given differences.

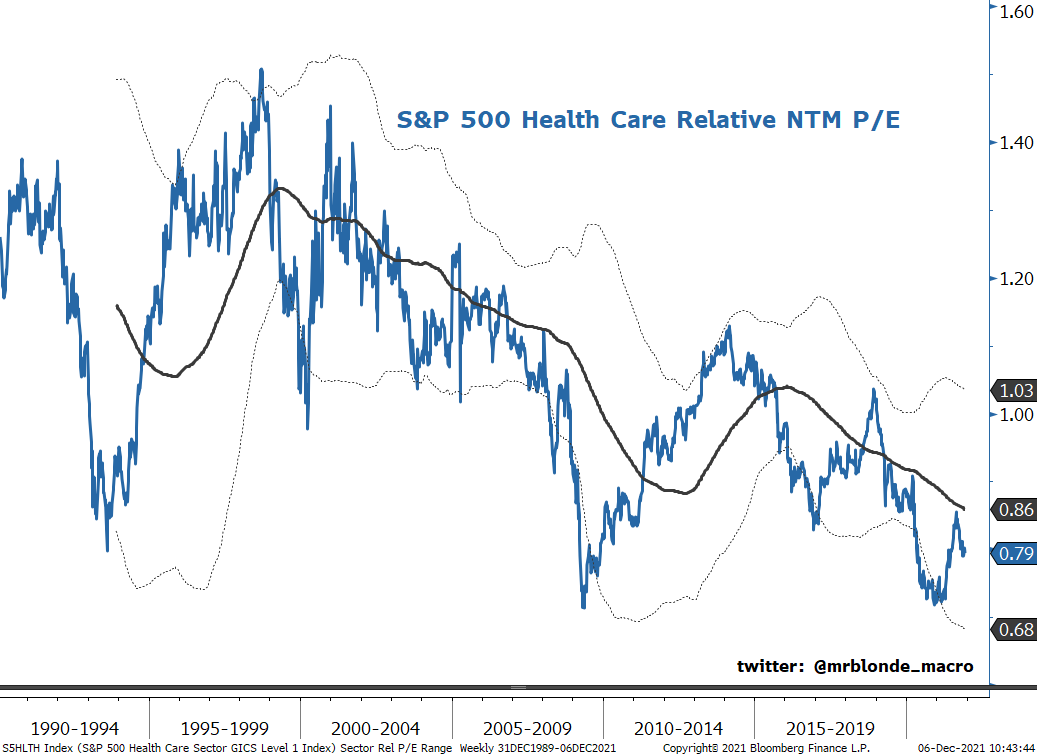

Healthy Opportunity

Along similar lines, Mr. Blonde finds the relative value per unit of fundamentals across the health care sector intriguing. Perhaps no other group exemplifies “quality value” more than the Health Care sector. Of course the group carries risk, primarily in the form of political risk, but trades at a 20% discount relative to the broad market this seems largely accounted for in price.

The sector offers well above market FCF yield, double digit sales growth and importantly low volatility of sales. This is before considering the secular forces of aging demographic, increased focus on health & well being and a global health pandemic. Mr. Blonde thinks health care has the characteristics to be an outperformer in 2022 — ‘cheap’ with good fundamentals.

A judgement call on Mr. Blonde’s part, but relative earnings for health care sector appear poised to inflect higher which can support outperformance. This view is supported by peaking cyclical growth and view for slowing pace of market earnings growth as 2022 progresses. Slowing elsewhere will favor the stability of the health care sector.

The stock list above is filled with stocks from the health care sector that offer attractive fundamentals for the expected environment. Mr. Blonde would also reference his list of high quality growth compounders for health care stocks of interest.

Bank Your Base Metals

While bank stocks and financials historically don’t outperform the market around Fed tightening cycles, Mr. Blonde recognizes the sensitivity to interest rates and the possibility that this cycle might be a little different. Rather than carrying financials exposure outright, pairing it against a base metals short is more attractive.

Long financials vs. short metals & mining is a pair long US$ and would likely benefit from an environment where US growth outperforms China growth. In both late 2015 and late 2018 environments the pair performed exceptionally well. This idea was first mentioned here, in late Sept, and still applies today.

In addition to the above, Mr. Blonde still favors S&P 500 dividend futures and high quality growth compounders as well as shorts in low quality, high beta market segments including non-US broadly and consumer. Expect the next phase will bring an equity market with more chop and less trend. Good luck trading.