Feeling Fragile

Narrow markets are fragile markets — the case for tactical correction

Disclosure

The commentary and ideas here represent one person’s opinion and should not be considered investment advice. You need to evaluate your own risk tolerance, time horizon and skill level. Hopefully the commentary assists in your judgement and process, but you need to do your own due diligence and decide the best course of action.

Feeling Fragile

The average stock is performing far worse than “the market”. High beta cyclicals are lagging the broad market badly and continue to send signs something isn’t right on the cyclical growth front. Some might be tempted to buy the reflation dip but best to refrain as these trends typically persist more than a couple months. With Fed on verge of tapering (liquidity tightening), economic surprise indices negative and disappointing data points are piling up (Philly Fed, NY Empire, July US retail sales, China July activity data just last week). August flash PMIs up next where Mr. Blonde expects downticks.

Bad Breadth

The % of companies > their 200d moving average peaked earlier this year and negative momentum has increased recently. Non-US markets, particularly emerging markets, are downright ugly with only 55% of constituents trading above 200d average.

Greenspan was wrong about a lot, but think he had this one right:

"Moreover, it is just not credible that the US can remain an oasis of prosperity unaffected by a world that is experiencing greatly increased stress." -Alan Greenspan, 9/4/98

Big Levels in Key Markets

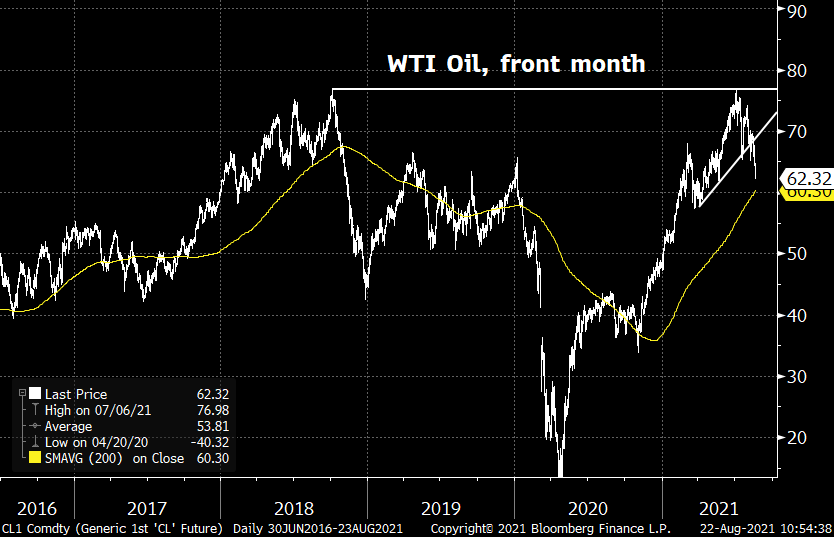

Complicating and confirming matters was the breakout in US$ and breakdown in oil last week. Mr. Blonde isn’t a technician, but both US$ and oil charts look ominous. US$ held early 2018 low and breaking to the upside.

Quite the top in WTI oil futures…literally to the tick of the Oct’18 high. Eerily reminiscent of a market waking up to slowing cyclical growth at a time when Fed is talking taper (i.e. tightening). Despite the option expiry induced equity bounce, oil finished the week making new lows.

The move in US$ is particularly notable given its relationship with earnings revision momentum. And as discussed in prior post, earnings revision momentum is a key factor in equity price momentum.

Waning Confidence

President Biden’s Job Approval rating is cratering like a Cathie Wood holding. If “The Donald” were at the helm he’d be shifting the news cycle and pumping stocks which seems far less likely with “Joe Hiden.”

Its not uncommon for first year Presidents to see a fade in enthusiasm. Its also not uncommon to experience a material setback this time of year and stage in the seasonal composite. Buckle up.

Confidence is also waning among equity long/short hedge funds. Its been a difficult year for long positions that are lagging the broad market. Sure, short positions have helped mitigate this negative alpha but the average fund is running with net long exposure near decade highs. PnL pain is often a precursor to market pain.

Window of Weakness

S&P 500 (SPX) resilience is undeniable, but increasingly vulnerable as risk across markets weaken. Hyman Minsky is rolling his eyes somewhere after SPX has gone 200 trading days without a >5% pullback.

Mr. Blonde created an indicator to capture and measure divergence between SPX and cross-asset markets. It started registering extreme readings in mid July.

Past divergences led to subsequent weakness in SPX, not always immediate but often within 3mo window. When the magnitude of cross-asset market weakness is meaningful (i.e. z-score < -0.5) the likelihood and degree of SPX weakness is greater. The window of weakness is open through early Oct based on past experience.

How to Trade

First, given the ‘growing but slowing’ backdrop favor high quality longs vs. high beta shorts. This pair has worked, but will continue to work as long as cyclical growth is decelerating. In an environment of financial repression and passive investing competition, investors feel pressured to stay fully invested in equities and therefore the internal rotations can be more forceful.

An industry group breakdown of various ETFs shows how significant the cyclical skew is in high beta style when compared to the more defensively positioned nature of quality. Mr. Blonde also believes software group has many defensive properties (i.e. recurring revenue, pristine balance sheets) that make the group similar to classic defensives.

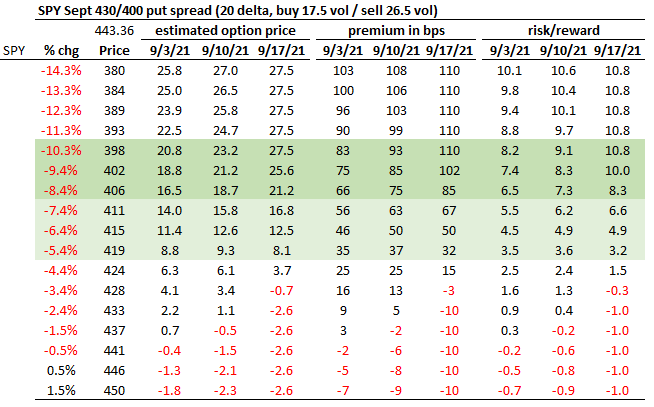

Second, buy SPX put protection in Sept for a broader market correction. Mr. Blonde wants to BTFD like everyone else, but need dry powder to do it. The above mentioned pressure to stay invested results in a market of fully invested bears. Downside volatility is elevated, but not extreme and notable its made series of higher lows since late 2017.

While implied volatility is far from highs, skew is elevated. Mr. Blonde believes this is partly structural as Treasuries no longer offer the same level of portfolio protection. The makes put spreads more attractive with the view for a modest correction (i.e. 5-10% range).

Markets are hard enough as it is, so Mr. Blonde likes to keep his portfolio hedges simple. SPY Sept 430/400 put spread is an attractive way to position for a modest market correction. Payout on premium risked ranges from 3.5-6x on 5-7% S&P 500 correction by mid-Sept and max payout of ~10x. Risking ~10bps premium of portfolio capital is currently equivalent to 3.5% SPY delta adjusted short position.

More aggressive traders may elect to leg into this option trade and buy the 430p today, while waiting to sell the 400p as the market corrects in order to improve on the estimated returns outlined in the table below.

Disclosure

The commentary and ideas here represent one person’s opinion and should not be considered investment advice. You need to evaluate your own risk tolerance, time horizon and skill level. Hopefully the commentary assists in your judgement and process, but you need to do your own due diligence and decide the best course of action.

Hi Mr.Blonde; thank you for taking the time to share your thoughts. I look forward to reading your future insights.

I find the options r/r table useful and would appreciate if you could share how to calculate estimated option price and premium in bps. Any links/resources that you recommend on that front would be greatly appreciated. Thank you and I hope to hear from you soon. Cheers.