This commentary remains free for all, but come 10/31 will require a monthly subscription. See here for details and expectations. Hopefully after reviewing content provided over the last year you will find it well worth the price.

In Bear Bounce? Mr. Blonde suggested the pre-conditions for a countertrend risk rally were in place. Shortly after, when everyone realized CSFB wasn’t Lehman 2.0, we posted one of the best two day gains in the last decade. Then faded and fell hard on what seemed to be a largely inline NFP report and the negativity returned in force. The bear bounce view has hardly been a no brainer, but seems to still have life.

Bear market rallies are typically vicious and don’t always jive with rational, fundamental explanation. They are primarily technical, positioning events. All of the ‘pre-conditions’ in the 9/30 commentary are still in place. Again, the fundamental core view remains the same (SPX to 3000-3200) and trading against one’s core view is uncomfortable, but we try our best to be unemotional and data-driven.

A few brief observations and then some ideas to consider.

Technically Speaking

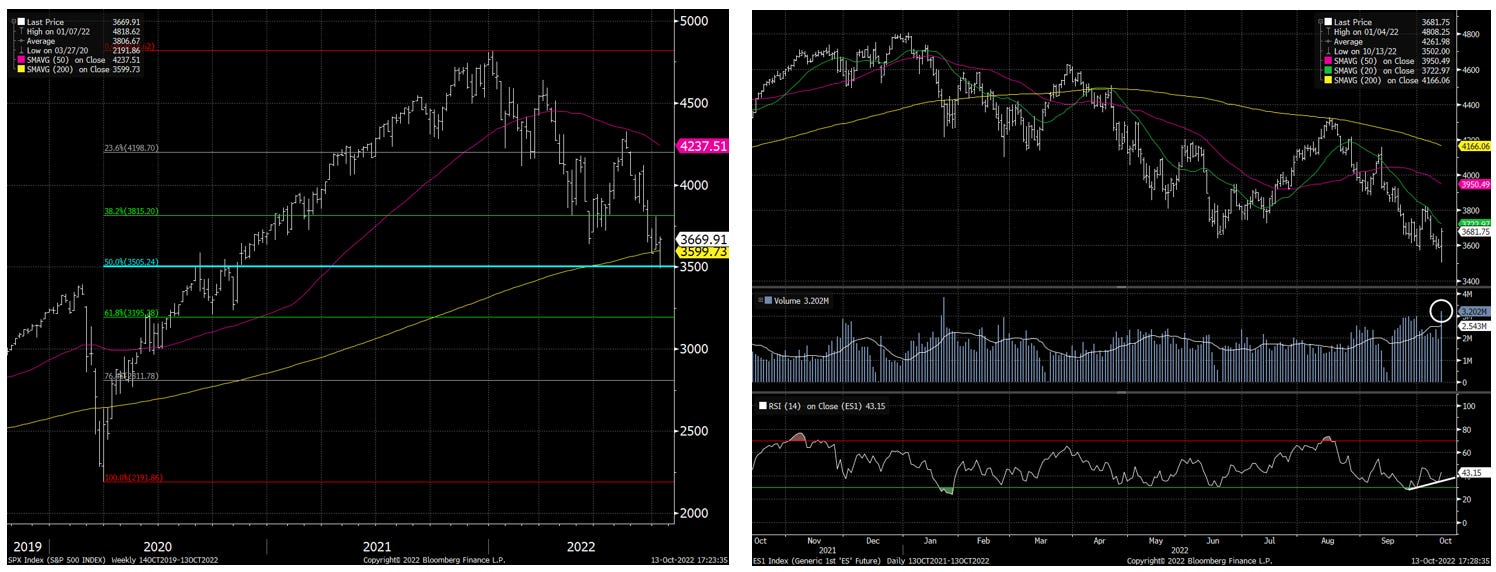

Visually, S&P 500 retraced 50% of the move from covid low and bounced hard to regain the also closely followed 200 week moving average. There was also a very large outside day reversal today and we closed strong on above average volume. The price can change tomorrow, but in the context of a disappointing CPI report markets held/regained important technical levels.

History Rhymes

In addition to the pre-conditions, the trading behavior today with the last time we started a bear rally has uncanny similarities both in timing and pattern. Since Sept quarter end, markets went up quickly only to fall into today’s CPI report…similar behavior in July. Both CPI reports experienced a sharp selloff, only to rally back hard on the same day. SPX futures retested and briefly undercut the June quarter end low and is showing similar pattern today. This a single sample and hardly rigorous analysis, but a reminder we’ve seen this behavior before…not long ago actually.

Mr. Blonde maintains Oct month end SPY call spread referenced in the Bear Bounce note and has added some Nov calls for some added leverage. If we get to next week without anymore UK pension drama the narrative can change. And don’t forget about the potential for pro-cyclical CTA flows.

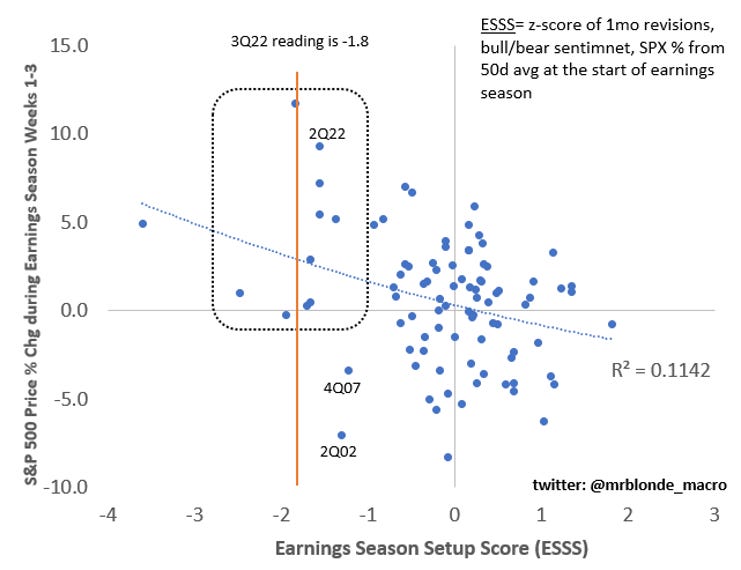

Earnings Season Setup

2Q earnings season was confusing. Pundits said earnings season was “good” and that’s why stocks went up, but when you actually study the facts to see numbers were cut meaningfully into the quarter and revisions coming out of the quarter were negative its hard to say it was good.

A better description may have been that 2Q results turned out better than feared. But how do we measure that fear? Mr. Blonde created the Earnings Seasons Setup Score (ESSS) to try to quantify this fear. The ESSS is an aggregate of revisions, survey sentiment, and measure of overbought/sold conditions.

Evaluating this measure at the start of each quarter from 1Q00 and comparing to market returns during the first few weeks of earnings season highlights how “better than feared” results can drive performance. Last quarter had a reading of -1.6 at the start of earnings season and entering tomorrow we are -1.8.

This analysis says nothing of Mr. Blonde’s fundamental outlook on earnings. This is about market expectations vs. what is delivered at this point in time. The ESSS and chart below simply suggest markets may already be braced for bad news.

Mr. Blonde will have more to say on 3Q earnings season in the coming week. The results won’t be great and corporate guidance is likely to be downbeat, but market conditions suggest we already know that. The earnings debate is no longer about direction, but severity and timing of that severity. Will it be 3Q? could be, but it could also slip into 4Q.

Are you gonna bark all day little doggie or are you gonna bite?

There is more than enough ‘bark’ each week with pundits pontificating about markets, their feelings and what markets should be. Mr. Blonde tries to dedicate time in each post to where there is ‘bite’ and interesting, relevant trades that can be added to a portfolio given current and expected market conditions.

Not every trade will be relevant to everybody, that’s just the reality of markets and the wide range of risk tolerances or time horizons. This is not a paper portfolio and not an outsourced portfolio of ideas to set and forget. As always, doing your own due diligence is highly recommended.

Short Eurostoxx 2023 Dividend Future

please note: 2023 dividend futures are paid out of 2022 profits — something Mr. Blonde misunderstood at the time of this idea. He incorrectly assumed the convention was similar to US dividend futures which payout when realized. This would make 2023 future less attractive short and favor 2024 future short, but 2024 is implying -10% growth and therefore a less compelling risk/reward. sorry for confusion.

A year ago, Mr. Blonde recommended S&P 500 dividend futures as an important alternative to long S&P 500 exposure with the opinion that a Fed rate hike cycle would likely significantly compress valuation multiples even as realized growth held up well. In a difficult year for most assets, this proved to be the right call:

Heading into 2023, the backdrop changed as fundamental growth risks are high and rising. Some weakness in profit growth was likely given overearning post COVID stimulus, but we now layered on significant financial conditions tightening and geopolitically driven energy price spikes that will further weigh on growth (here). Mr. Blonde likes to trade this risk by being short DEDZ3 futures (Eurostoxx 2023 dividend futures).

Currently 2023 dividend futures imply growth declines 5-6% in 2023, but could ultimately prove to be 3-4x. In europe, dividend growth and earnings growth are closely tied.

Europe earnings growth tends to be high beta relative to US given its exposure to global trade and more cyclical composition. Using the Macro Growth Composite as a guide suggests y/y Europe earnings growth down 20% or more. This is consistent with the relationship of y/y M1 and Europe PMIs as presented by the must follow @IanRHarnett and @asr_london of Absolute Strategy Research.

Eurostoxx is likely to perform poorly in such a scenario, but with the index already trading at 10x forward p/e it may not offer the desired asymmetry and history suggests equity prices bottom 6-9mos before EPS bottoms.

Bottom line, short DEDZ3 (ticker: DESX5 on interactive brokers) as the next phase of the market correction is primary about earnings disappointment.

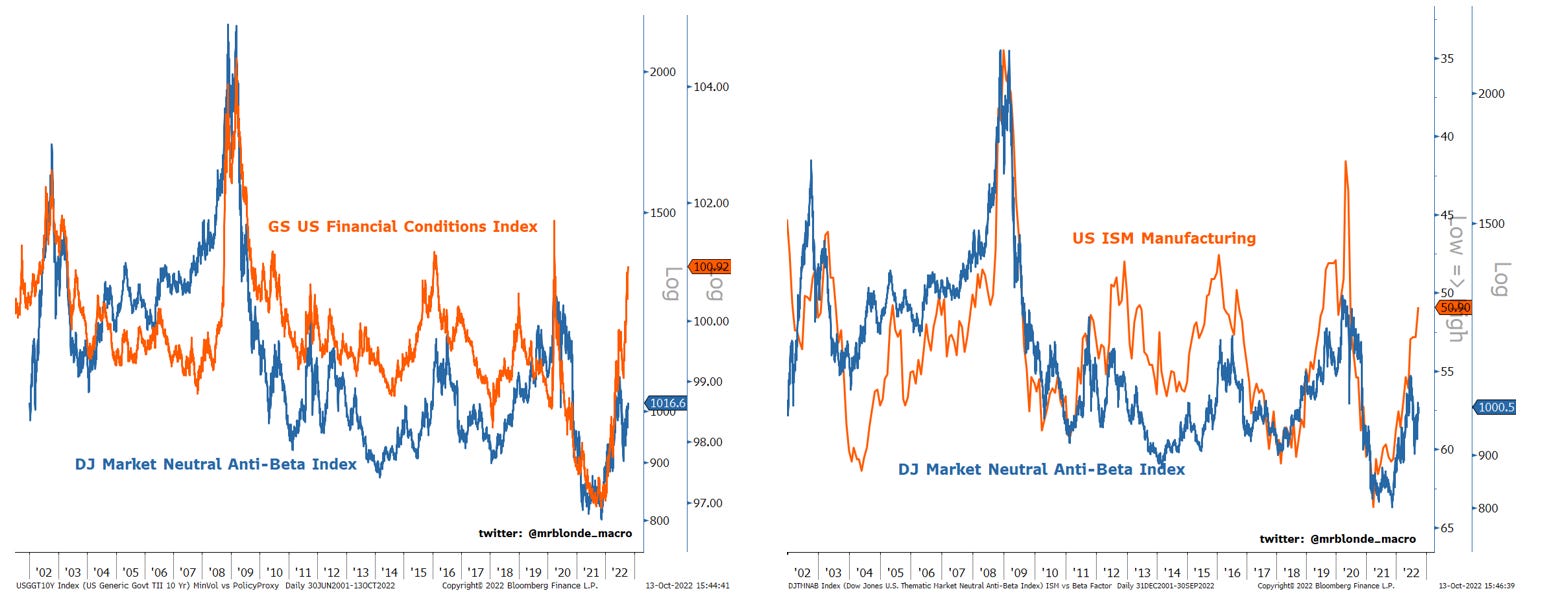

Long Low Risk

A repeat idea that still has merit. In fact, the investment case has strengthened with another wave of financial conditions tightening and ISM falling to 50.9. As fundamental conditions weaken following the sharp tightening of financial conditions we will see companies with high volatility, cyclical cash flows come under great pressure. This pair trade is long the lowest beta and short the highest beta stocks within each sector across the market.

Mr. Blonde continues to see this as a way to be long volatility without paying the negative carry associated with long volatility (i.e. VIX futures). For institutional investors most dealers offer a relevant equity swap pair to reflect this view, while retail traders can position via BTAL ETF (AGFIQ US Market Neutral Anti-Beta Fund).

Utility Value

This idea was shared last in Bear Bounce? . Needless to say, the underperformance last week was incredibly frustrating. It’s of course possible we end up in the 20% of cases when some mean reversion doesn't work, but empirical odds suggest XLU higher in a month (historically its higher 80-88% of the time from such oversold conditions). So, Mr. Blonde hates the outcome so far, but he doesn’t regret the buy decision.

Not certain, but suspect some of the recent selling pressure may be related to retail boomer selling and/or a low volatility equity unwind (see weakness in REITs, WM, RSG, JNJ, KO, SPLV, etc.) perhaps UK pension funds?

This signal first hit last Friday with a reading of -3.1 and -4.7 yesterday. Giving this one a bit more time to work.

Software over Semis…Still

The tech sector is incredibly controversial given its long period of outperformance and ownership. Long software / short semis is a pair first suggested in late Jan’22. The view at the time was to capitalize on oversold conditions in a pair trade that historically performs well during periods of negative cyclical growth momentum (falling ISM). Within the tech sector this is a play on defensive/cyclical as semis are far more exposed to goods sector, inventory gluts and global trade disruptions. Software’s main issue is it was expensive and over-owned, but after the sharp sell off at the turn of the year this risk seems to be in a better place…at least relative to other tech groups.

It’s too early to be confident, but Mr. Blonde thinks this has the potential to be an important pair in 2023 if the recession forecasts come to fruition and growth takes over from inflation as the driver of rates.

Bottom line, long software (IGV) and short semis (SMH) has an improving technical picture, the right characteristics for slowing growth environment and in a scenario where yields stalled out or fell could remove a macro pressure point.

That’s all for now. If you appreciate these insights please like, comment and/or share. Planning a 3Q earnings season preview sometime in the next week and will comment on the bear bounce view if conditions change.

Thanks for your insightful work, as usual.

A quick remark though on Sx5e dividends. If you want to play a correction in Eps, then it’s not dedz3 I’d short, but dedz4.

Dedz3 is a future on dividends paid in 2023 out of 2022 eps, which we already have rather goid visibility on. Q3 will be ok (cf no big pre-announcements), so, bar an horrible Q4, 2022 eps will be ok.

So imho the only way dedz3 really corrects is a bet on a wave of windfall taxes from gvt on banks/energy/utility names. This may happen, but is a totally different bet from your fundamentally bearish european equities eps trajectory.

Sharing your view on eps, I’d sell dedz4, as to me the main risk is on 2023 eps.

Mike Wilson seems to have the same targets as you have.